Planning for retirement can feel like navigating a complex maze, especially when faced with choices like a 403(b) and a 401(k)․ Both are employer-sponsored retirement savings plans designed to help individuals build a secure financial future, but they cater to different sectors and have nuanced differences․ Understanding these distinctions is crucial for making informed decisions that align with your specific circumstances and retirement goals․ This article will delve into the intricacies of 403(b) Vs 401k, comparing their features, eligibility requirements, and investment options to help you determine which plan might be a better fit for you․

Understanding the Core Differences

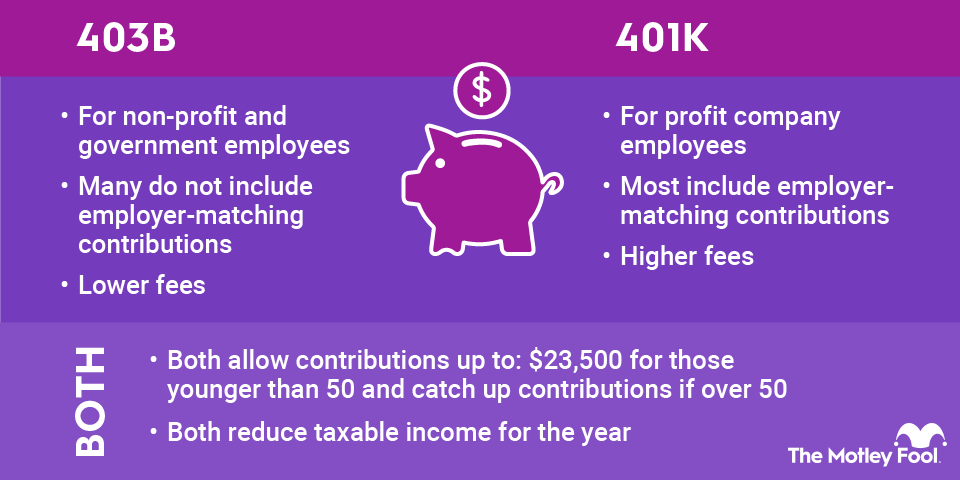

While both 403(b) and 401(k) plans share the fundamental goal of helping you save for retirement, their key differences lie in who is eligible to participate and the types of investments offered․

Eligibility: Who Can Participate?

- 403(b) plans: Primarily offered to employees of public schools, universities, hospitals, and certain non-profit organizations (501(c)(3) organizations)․

- 401(k) plans: Generally offered to employees of for-profit companies, but may also be available to some non-profit organizations․

Investment Options: Where Does Your Money Go?

The investment options available within each plan can also differ․ While both typically offer a range of mutual funds, 403(b) plans may also include annuity contracts․

- 403(b) plans: Often feature a mix of mutual funds and annuity contracts․ Annuities offer a guaranteed stream of income in retirement, but they can also come with higher fees․

- 401(k) plans: Primarily offer a wider variety of mutual funds, potentially including index funds, target-date funds, and actively managed funds․

Contribution Limits and Tax Advantages

The contribution limits for both 403(b) and 401(k) plans are generally the same, and they are subject to change annually by the IRS․ Both plans offer pre-tax contributions, meaning your contributions are deducted from your paycheck before taxes are calculated, potentially lowering your current taxable income․ Taxes are then deferred until retirement when you begin taking distributions․ Roth options may also be available for both plans, allowing for after-tax contributions with tax-free withdrawals in retirement․

Catch-up contributions are also permitted for those age 50 and older, allowing them to contribute even more to their retirement savings․

Fees and Expenses

Fees and expenses are an important consideration when choosing a retirement plan․ These fees can eat into your investment returns over time, so it’s crucial to understand what you’re paying․

Both 403(b) and 401(k) plans may charge administrative fees, investment management fees (expense ratios for mutual funds), and other related expenses․ It’s essential to review the fee disclosures for each plan to compare costs and determine which offers the most cost-effective investment options․

Making the Right Choice for You

Ultimately, the best retirement plan for you depends on your individual circumstances, employment situation, and risk tolerance․ If you work for a public school, university, hospital, or qualifying non-profit, a 403(b) may be your only option․ However, if you have a choice between a 403(b) Vs 401k, carefully consider the investment options, fees, and potential for employer matching contributions․

Consider your risk tolerance and investment goals when evaluating the available investment options․ Do you prefer a guaranteed income stream in retirement (annuities) or a wider range of mutual fund choices? Also, be sure to understand the fees associated with each plan․ Finally, seeking professional financial advice is always a good idea to ensure you’re making the best decisions for your long-term financial security․ Choosing between a 403(b) and 401(k) requires careful consideration, but by understanding the key differences and evaluating your own needs, you can make an informed decision that sets you on the path to a comfortable retirement․ Remember, the most important thing is to start saving early and consistently, regardless of which plan you choose․ And as you approach retirement, understanding the best strategy for 403(b) Vs 401k income distribution is essential․

As you can see, the decision of whether to choose a 403(b) Vs 401k depends on your specific situation, but hopefully this article has provided helpful insights to guide you․