Credit insurance‚ a product often offered alongside loans‚ promises to protect borrowers against unforeseen circumstances that might hinder their ability to repay their debt. This type of insurance typically covers events such as job loss‚ disability‚ or even death‚ ensuring that the loan balance is either partially or fully paid off. Many consumers find themselves facing the question of whether to accept or decline this add-on‚ especially considering its impact on the overall cost of borrowing. Understanding the nuances of credit insurance and evaluating individual financial circumstances are critical steps in making an informed decision. Is credit insurance truly a safety net‚ or an unnecessary expense?

Understanding Credit Insurance

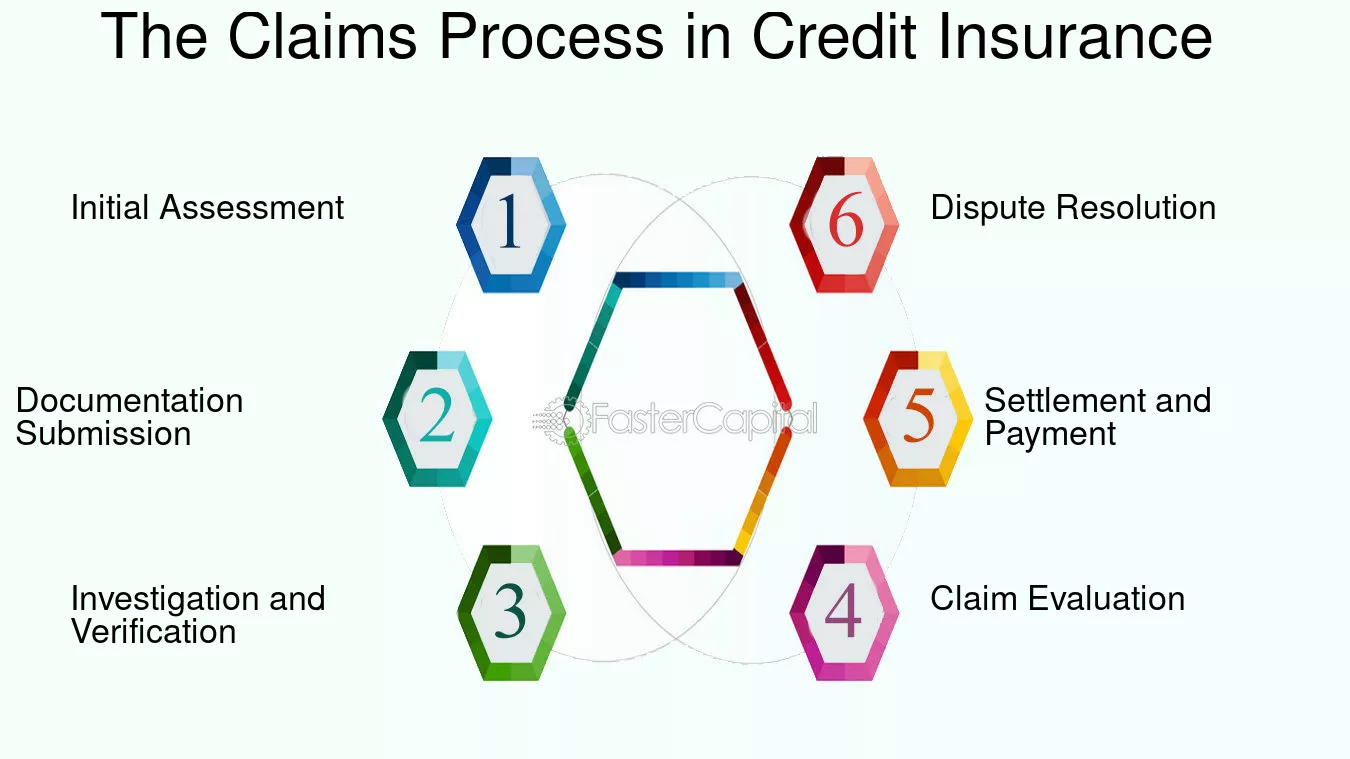

Credit insurance aims to provide a safety net for borrowers‚ covering loan payments when unexpected life events occur. It’s essentially a form of debt protection‚ transferring the risk of non-payment from the borrower to the insurance provider. However‚ it’s important to understand the different types of credit insurance and their specific coverage details.

Types of Credit Insurance

- Credit Life Insurance: Pays off the loan balance in the event of the borrower’s death.

- Credit Disability Insurance: Covers loan payments if the borrower becomes disabled and unable to work.

- Credit Unemployment Insurance: Covers loan payments if the borrower loses their job involuntarily.

- Credit Property Insurance: Protects collateral used to secure the loan (e.g.‚ a car).

The Pros and Cons of Credit Insurance

Deciding whether or not to purchase credit insurance involves weighing its potential benefits against its costs and limitations. While it can offer peace of mind‚ it’s essential to consider alternative options and assess your individual risk profile.

Advantages

- Financial Protection: Provides a safety net during difficult times‚ preventing loan default and potential damage to your credit score.

- Peace of Mind: Offers reassurance that your debt will be covered in the event of unforeseen circumstances.

- Convenience: Simplifies the process of managing debt in the event of job loss‚ disability‚ or death.

Disadvantages

- Cost: Credit insurance can significantly increase the overall cost of borrowing.

- Limited Coverage: Policies often have exclusions and limitations‚ such as waiting periods or pre-existing condition clauses.

- Overlapping Coverage: You may already have adequate protection through existing life‚ disability‚ or unemployment insurance policies.

- Alternatives Exist: Creating an emergency fund or exploring other insurance options may be more cost-effective.

Is Refusing Credit Insurance the Right Choice?

Ultimately‚ the decision to refuse or accept credit insurance depends on your individual circumstances‚ financial situation‚ and risk tolerance. Before making a choice‚ carefully evaluate your existing insurance coverage‚ consider the cost of the policy‚ and understand the specific terms and conditions.

To help you visualize the comparison:

| Feature | Credit Insurance | Alternative Options (e.g.‚ Emergency Fund‚ Existing Insurance) |

|---|---|---|

| Cost | Adds to the loan principal‚ increasing overall borrowing costs. | Requires upfront investment and ongoing maintenance. |

| Coverage | Specific to the loan; may have limitations and exclusions. | May offer broader coverage and greater flexibility. |

| Convenience | Automatically included with the loan; simplifies claims process in some cases. | Requires proactive management and understanding of policy terms. |

| Portability | Not portable; tied to the specific loan. | Portable; can be used for various financial needs. |

The question of whether or not to refuse credit insurance is a personal one‚ and it should be based on a thorough understanding of your financial situation and risk tolerance. Assess your existing coverage‚ weigh the costs and benefits‚ and make an informed decision that aligns with your long-term financial goals. Ultimately‚ understanding the implications of credit insurance is key to making the right choice for you.