The idea that all debts magically disappear from your credit report after seven years is a common misconception. While there’s truth to the seven-year rule‚ it’s more nuanced than it seems. Understanding the intricacies of credit reporting is crucial for maintaining a healthy credit score and financial well-being. Let’s delve into the details of what disappears‚ what sticks around‚ and what you need to know about managing your credit history effectively. This article explores the lifespan of debts on your credit report and clarifies what you should expect.

The 7-Year Rule: What Actually Disappears?

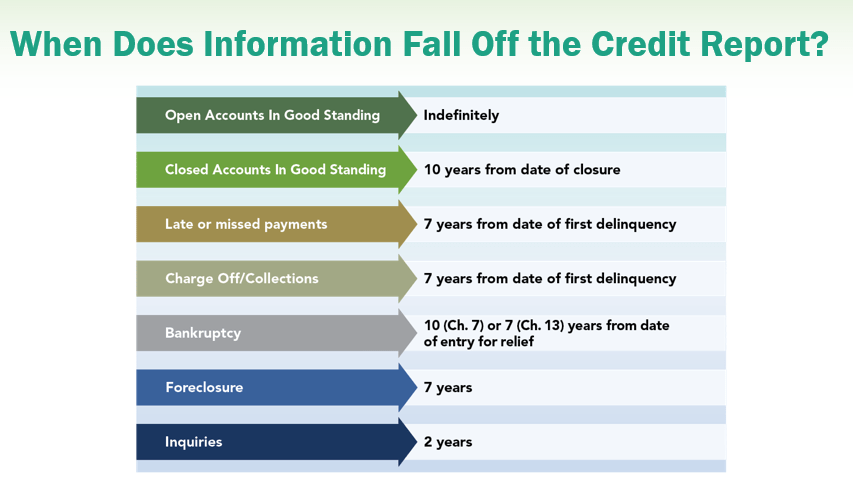

This section details the types of negative information that are generally removed after seven years.

- Most Negative Information: Late payments‚ collections accounts‚ and charged-off debts typically fall off your credit report after seven years from the date of the first delinquency (the date you first missed a payment).

- Chapter 7 Bankruptcy: Stays on your credit report for 10 years from the filing date.

- Chapter 13 Bankruptcy: Remains on your credit report for 7 years from the filing date.

- Inquiries: Hard inquiries from credit applications generally disappear after two years.

Exceptions to the 7-Year Rule and Other Factors

Not all negative information disappears after seven years. Here’s what can remain and why.

Certain types of information can remain on your credit report longer than seven years‚ impacting your credit score for an extended period. Here’s a breakdown:

| Information Type | Reporting Period |

|---|---|

| Chapter 7 Bankruptcy | 10 years from filing date |

| Unpaid Tax Liens | Indefinitely (unless paid) |

| Judgments (Unpaid) | Varies by state‚ often longer than 7 years |

| Student Loans (Unpaid) | Can remain indefinitely |

State Laws and Statute of Limitations

State laws play a role in how long a debt can be legally pursued‚ but this is separate from credit reporting. Know your state’s rules.

The statute of limitations on debt refers to the time limit a creditor has to sue you to collect a debt. This varies by state and type of debt. Understanding your state’s laws is important for protecting yourself legally. However‚ keep in mind that even if a debt is past the statute of limitations‚ it can still appear on your credit report for up to seven years from the date of first delinquency.

Debt Validation and Credit Repair

You have the right to validate debts and challenge inaccurate information on your credit report.

If you believe information on your credit report is inaccurate or incomplete‚ you have the right to dispute it with the credit bureaus. This process can potentially lead to the removal of incorrect information‚ even if it hasn’t reached the seven-year mark. Sending a debt validation letter to the collection agency can force them to provide proof of the debt. If they cannot‚ the debt may be removed.

FAQ: Debts and Your Credit Report

Here are some frequently asked questions regarding debts and credit reporting.

- Q: Will paying off a debt remove it from my credit report immediately?

A: No‚ paying off a debt doesn’t automatically remove it. The negative record will still remain for up to seven years. However‚ a paid debt looks better than an unpaid one. - Q: What happens if a debt is sold to a new collection agency?

A: The original delinquency date still applies. The new collection agency cannot reset the clock. - Q: How can I check my credit report for errors?

A: You can obtain a free copy of your credit report from each of the three major credit bureaus (Equifax‚ Experian‚ and TransUnion) once a year at AnnualCreditReport.com. - Q: Is it worth using a credit repair company?

A: You can do everything a credit repair company does yourself for free. Be wary of companies making unrealistic promises.

Understanding how long debts stay on your credit report is essential for managing your financial health. While the seven-year rule offers some relief from past financial mistakes‚ it’s crucial to remember the exceptions and take proactive steps to monitor and correct your credit report. Paying debts on time‚ keeping credit utilization low‚ and regularly reviewing your credit reports are vital for maintaining a good credit score. Remember that building a positive credit history takes time and effort‚ but it’s an investment that pays off in the long run. Taking control of your finances and understanding the intricacies of credit reporting is empowering and can lead to better financial opportunities in the future. Don’t hesitate to seek professional financial advice if you need assistance navigating complex credit issues.

Beyond the Seven-Year Mark: Rebuilding Your Credit

Even after negative information falls off your credit report‚ it’s crucial to focus on rebuilding your creditworthiness. This involves establishing positive credit habits and demonstrating responsible financial behavior to lenders.

Think of your credit report as a living document that reflects your financial responsibility. While the past may fade‚ the future is yours to shape. Here are some key strategies for building a solid credit foundation:

- Make On-Time Payments: This is the single most important factor in your credit score. Set up automatic payments or reminders to ensure you never miss a due date.

- Keep Credit Utilization Low: Aim to use no more than 30% of your available credit on each credit card. Lower is even better.

- Diversify Your Credit Mix: Having a mix of credit accounts (e.g.‚ credit cards‚ installment loans) can positively impact your credit score. However‚ don’t open new accounts just for the sake of diversification.

- Become an Authorized User: If you have a trusted friend or family member with a credit card in good standing‚ becoming an authorized user on their account can help build your credit history.

- Consider a Secured Credit Card: If you have limited or damaged credit‚ a secured credit card can be a good way to start building credit. You’ll need to put down a security deposit‚ which typically serves as your credit limit.

The Psychology of Credit: A Mindset Shift

Credit isn’t just about numbers; it’s also about cultivating a healthy relationship with money and understanding your spending habits. A shift in mindset can lead to lasting positive changes.

Before applying for any new credit‚ ask yourself: Do I really need this? Can I afford it? Avoid impulse purchases and carefully consider the long-term implications of taking on debt. Budgeting and financial planning are essential tools for managing your finances effectively and preventing future credit problems. Remember‚ responsible credit use is a marathon‚ not a sprint. Consistency and discipline are key to long-term success.

Beware of Credit Repair Scams

Legitimate credit repair takes time and effort. Be wary of companies promising quick fixes or guaranteed results.

If a credit repair company promises to remove accurate negative information from your credit report‚ it’s likely a scam. Only time and responsible credit behavior can truly repair your credit. Avoid companies that ask for upfront fees before providing any services or that encourage you to lie on credit applications. These practices are illegal and can harm your credit even further. Remember‚ you have the right to dispute inaccurate information on your credit report yourself‚ for free‚ through the credit bureaus.

FAQ: More Credit Rebuilding Questions

Let’s address some more common questions about rebuilding your credit after negative marks have fallen off.

- Q: How long does it take to rebuild credit?

A: It depends on the severity of your past credit problems and how consistently you practice good credit habits. It can take several months to a year or more to see significant improvements. - Q: Will closing old credit accounts help my credit score?

A: Closing old credit accounts can sometimes hurt your credit score‚ especially if they are your oldest accounts or have available credit that you are using. Consider the impact on your credit utilization before closing any accounts. - Q: What is a credit score simulator?

A: Credit score simulators can help you understand how different actions‚ such as paying down debt or opening a new credit card‚ might affect your credit score. However‚ keep in mind that these are just estimates. - Q: Should I consolidate my debt?

A: Debt consolidation can be a good option if you can secure a lower interest rate than you are currently paying. However‚ be sure to consider any fees associated with consolidation and whether you are truly addressing the underlying spending habits that led to the debt in the first place;

Rebuilding your credit after negative information has been removed is a journey that requires patience‚ discipline‚ and a commitment to responsible financial habits. By focusing on making on-time payments‚ keeping credit utilization low‚ and avoiding new debt‚ you can gradually improve your credit score and open doors to better financial opportunities. Remember to be proactive in monitoring your credit report for errors and taking steps to correct any inaccuracies. With time and effort‚ you can achieve a healthy credit score and a brighter financial future. Don’t be discouraged by setbacks; stay focused on your goals and celebrate your progress along the way. Seeking guidance from a qualified financial advisor can also provide valuable support and personalized strategies for your credit rebuilding journey.