Applying for an Economic Injury Disaster Loan (EIDL) can be a critical step for small businesses facing financial hardship. Navigating the application process often involves questions about banking requirements‚ and one common concern is whether a dedicated business bank account is necessary. Understanding the specific guidelines set by the Small Business Administration (SBA) regarding bank accounts is crucial for a smooth and successful EIDL application and disbursement. Let’s delve into the requirements and considerations surrounding business bank accounts for EIDL loans.

Understanding EIDL Loan Requirements and Bank Accounts

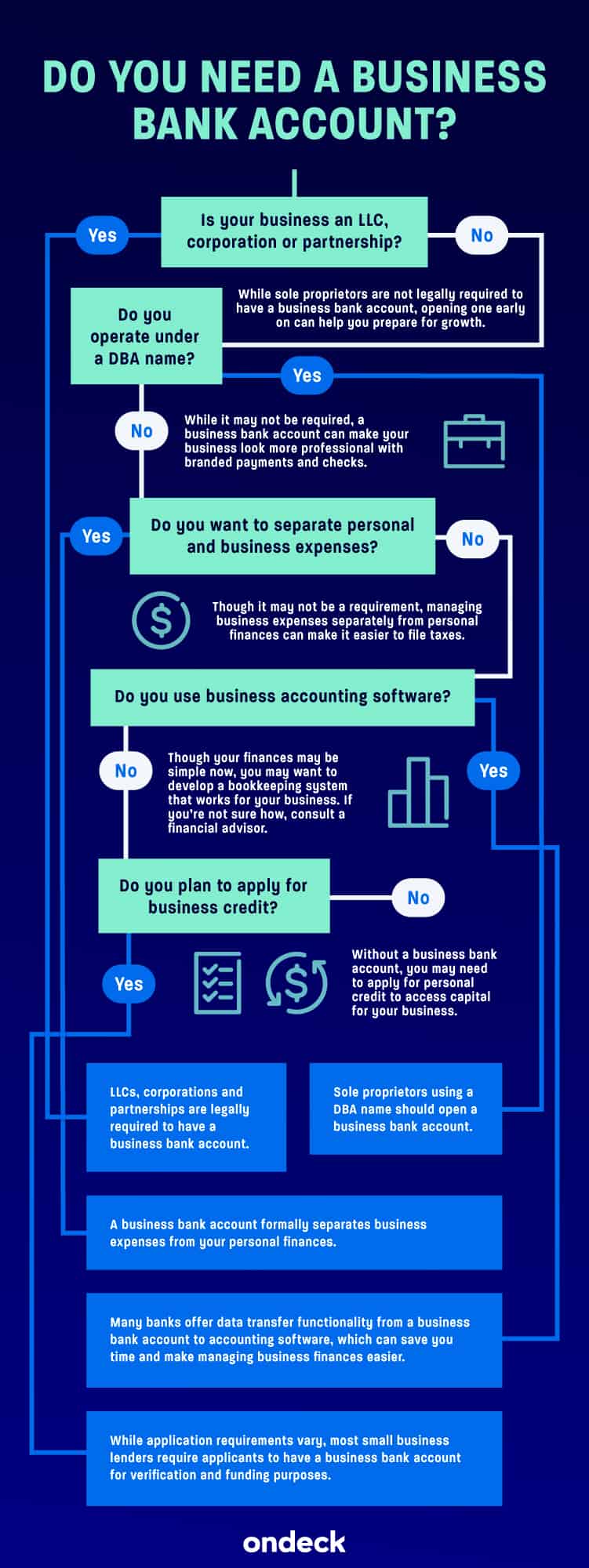

Before diving into specifics‚ it’s essential to understand that the SBA has requirements surrounding how loan proceeds are handled. This often ties into the need for a business bank account.

The SBA typically requires EIDL funds to be deposited into a separate account‚ usually a business bank account‚ to ensure proper tracking and use of the funds. This helps in maintaining transparency and prevents the commingling of loan proceeds with personal finances. Below is some supporting information:

- Transparency: A business bank account provides a clear record of all EIDL-related transactions.

- Compliance: Using a separate account facilitates compliance with SBA regulations.

- Audit Trail: Having a dedicated account creates a clear audit trail for potential future audits.

When is a Business Bank Account Absolutely Necessary?

While the SBA often encourages or requires a business bank account‚ certain circumstances make it an absolute necessity.

The following table outlines situations where a business bank account is generally required for an EIDL loan:

| Situation | Requirement | Reason |

|---|---|---|

| Operating as a Corporation‚ LLC‚ or Partnership | Almost Always Required | These business structures are legally separate from their owners‚ necessitating a separate bank account. |

| Receiving a Large EIDL Loan (Specific Dollar Amount Varies) | Likely Required | The SBA may mandate a separate account for larger loan amounts to ensure proper fund management. Check with SBA for specifics on current requirements. |

| Mixing Business and Personal Finances | Strongly Recommended | Even if not strictly required‚ it’s highly advisable to separate funds to maintain accurate records and avoid complications. |

Alternatives if You Don’t Have a Business Bank Account

If you don’t already have a business bank account‚ opening one before applying for an EIDL loan is generally the best course of action.

While opening a business bank account is the preferred method‚ some borrowers may explore alternatives‚ although these are generally not recommended by the SBA:

- Using a Sole Proprietorship Personal Account (Not Recommended): If operating as a sole proprietorship‚ some lenders may allow using a personal account‚ but this is strongly discouraged due to the risk of commingling funds.

- Opening a Separate Sub-Account: Some banks offer the option of creating a sub-account within your existing personal account‚ dedicated solely to EIDL funds. This is a less ideal solution.

FAQ: EIDL Loans and Bank Accounts

Here are some frequently asked questions about EIDL loans and the requirement for business bank accounts.

- Q: Can I use my personal bank account for an EIDL loan? A: Generally‚ no‚ especially if you operate as a corporation‚ LLC‚ or partnership. Even as a sole proprietor‚ a business bank account is highly recommended.

- Q: What if I don’t have a business bank account when I apply? A: It’s best to open one before applying. The SBA may require it as a condition of loan approval.

- Q: What type of business bank account do I need? A: Any standard business checking account will typically suffice. Check with your bank to ensure it meets the SBA’s requirements.

- Q: How soon should I open a business bank account after applying for an EIDL loan? A: As soon as possible. Having the account open demonstrates preparedness and can expedite the loan approval process.

While the focus is often on having a business bank account‚ the type of account also warrants consideration. A basic business checking account will typically suffice for managing EIDL funds. However‚ businesses might explore options that offer additional benefits‚ such as interest-bearing accounts (though interest earned might need to be reported and managed separately according to SBA guidelines) or accounts with integrated accounting software features. The key is to choose an account that facilitates easy reconciliation and reporting‚ simplifying the process of demonstrating proper use of loan proceeds to the SBA‚ if requested.

Maintaining Accurate Records: A Crucial Component

The establishment of a business bank account is merely the first step; diligent record-keeping is paramount throughout the loan term. The SBA emphasizes the importance of maintaining meticulous records related to all transactions involving EIDL funds. This includes documenting expenses‚ tracking revenues generated through the use of the loan‚ and retaining receipts for all purchases made with the loan proceeds. Such records not only ensure compliance with SBA regulations but also provide valuable insights into the effectiveness of the EIDL loan in supporting the business’s recovery.

Consider these record-keeping best practices:

- Utilize Accounting Software: Implement accounting software to streamline the process of tracking income and expenses.

- Maintain Digital Copies: Scan and store digital copies of all receipts and invoices.

- Regular Reconciliation: Reconcile bank statements with accounting records on a regular basis (e;g.‚ monthly).

- Categorize Expenses: Accurately categorize all expenses to demonstrate how the loan funds were used.

Potential Consequences of Non-Compliance

Failure to comply with the SBA’s requirements regarding the use and documentation of EIDL funds can have serious consequences.

The following highlights the potential ramifications of non-compliance:

- Loan Recall: The SBA may demand immediate repayment of the outstanding loan balance.

- Legal Action: The SBA may pursue legal action to recover the loan funds.

- Ineligibility for Future SBA Loans: Non-compliance can disqualify a business from receiving future SBA loans or assistance programs.

Seeking Professional Advice

Navigating the complexities of EIDL loan requirements and compliance can be challenging‚ particularly for small business owners who may lack extensive financial expertise. Consulting with a qualified accountant or financial advisor can provide invaluable guidance. A professional can help businesses establish appropriate accounting practices‚ ensure compliance with SBA regulations‚ and develop strategies for effectively managing EIDL funds to maximize their impact on the business’s recovery.

The Importance of Proactive Communication

Throughout the EIDL loan term‚ maintaining open and proactive communication with the SBA is crucial. If a business encounters unforeseen challenges or anticipates difficulty in meeting its loan obligations‚ it should promptly contact the SBA to discuss potential solutions. The SBA may be willing to work with borrowers to adjust repayment terms or explore other options to help them avoid default. Transparency and proactive communication can demonstrate a borrower’s good faith and increase the likelihood of finding a mutually agreeable resolution.

Therefore‚ while a business bank account may not be explicitly mandated in every EIDL loan scenario‚ its strategic value in facilitating compliance‚ ensuring transparency‚ and promoting responsible financial management makes it an indispensable tool for borrowers. Furthermore‚ paired with meticulous record-keeping and proactive communication with the SBA‚ a business can effectively leverage an EIDL loan to overcome financial hardship and achieve sustainable growth.