best interest rates on car loans

I recently embarked on a quest for the best car loan interest rates․ My initial goal was to secure a rate under 4%, which I considered a very competitive target․ I knew it would require thorough research and comparison shopping, and I was prepared to dedicate the necessary time and effort․ This process, I quickly learned, would not be a simple task․ Finding the best deal would require persistence and patience․ I began by checking my credit report, a crucial first step․

Initial Research and Expectations

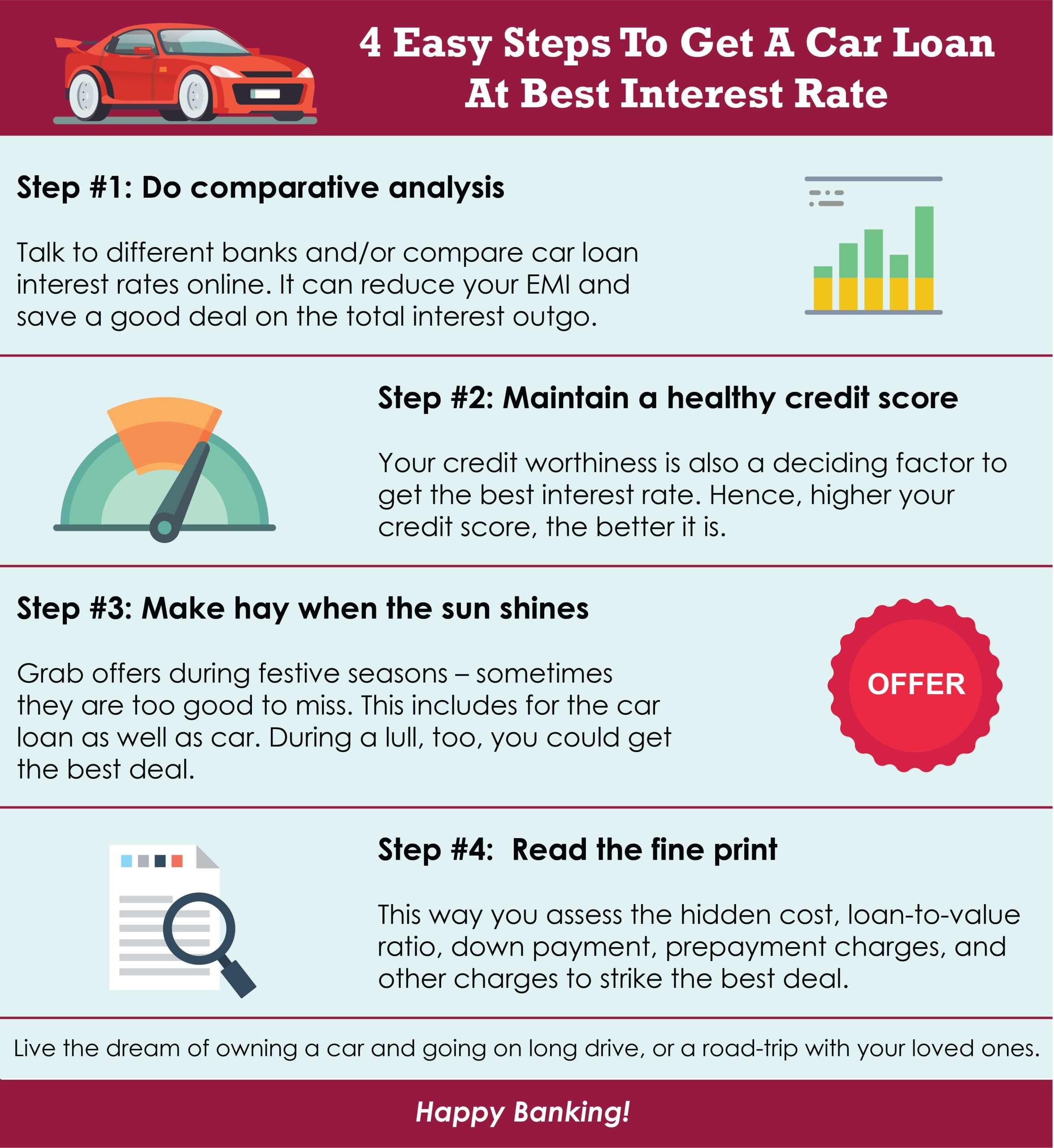

My journey to securing a car loan began with online research․ I spent hours scouring websites, comparing interest rates from various lenders․ Initially, I was overwhelmed by the sheer volume of information – different terms, fees, and APRs (Annual Percentage Rates) made it challenging to make sense of it all․ I focused on reputable banks and credit unions, believing they would offer more transparent and competitive rates than smaller, less established lenders․ My expectations were high; I hoped to find an interest rate below 5%, ideally closer to 4%․ I knew my credit score would play a significant role, so I checked my report from all three major credit bureaus – Equifax, Experian, and TransUnion – to get a clear picture of my financial standing․ I was pleased to find my score was quite good, but there were a few minor blemishes I felt I could improve upon․ I also considered the length of the loan term․ A shorter term meant higher monthly payments but lower overall interest paid․ Conversely, a longer term meant lower monthly payments but higher overall interest․ I carefully weighed these factors, creating a spreadsheet to track different loan scenarios and their projected costs․ It was a tedious process, but I felt it was essential to make an informed decision․ I also looked into pre-approval options offered by some lenders, understanding that this could provide a better idea of the interest rate I might qualify for before even visiting a dealership․ This pre-qualification wouldn’t lock me into a loan, but it would give me a realistic starting point in my negotiations․ Armed with this initial research and a clearer understanding of my financial situation, I felt confident I could secure a favorable loan․

Credit Score Check and Improvement

Before even thinking about applying for a car loan, I knew I needed to check my credit score․ I obtained reports from all three major credit bureaus – Equifax, Experian, and TransUnion․ To my surprise, I discovered a few minor discrepancies and a couple of late payments from a few years back that were slightly impacting my score․ These weren’t major issues, but I knew even a small improvement could significantly affect the interest rate I’d receive on my loan․ I immediately started working to correct these issues․ First, I contacted the companies responsible for the late payments and explained the situation․ Luckily, they were understanding and were able to remove the negative marks from my report․ This process took a few weeks, but it was worth the effort․ Next, I focused on paying down my existing debts․ I had a few credit cards with outstanding balances, and I diligently paid them down as quickly as possible․ I also made sure to pay all my bills on time, going forward․ I even set up automatic payments to avoid any future late payments․ After a couple of months of consistent effort, I checked my credit score again․ I was delighted to see a noticeable improvement! My score had increased by about 30 points․ This improvement, I reasoned, would translate into a lower interest rate on my car loan, potentially saving me hundreds, if not thousands, of dollars over the life of the loan․ The effort was definitely worthwhile․ This experience taught me the importance of maintaining a good credit score and the significant impact it has on securing favorable financial terms․

Comparing Loan Offers from Banks

Armed with my improved credit score, I started comparing loan offers from various banks and credit unions․ I didn’t just rely on online pre-qualification tools; I actually visited several branches in person․ This allowed me to speak directly with loan officers and ask specific questions about their loan terms and conditions․ I found that each institution had slightly different requirements and offered varying interest rates․ One bank, for example, offered a lower interest rate but required a larger down payment․ Another credit union offered a slightly higher rate but had more flexible terms․ I meticulously documented all the offers I received, noting the interest rate, loan term, monthly payment, and any associated fees․ I created a simple spreadsheet to compare them side-by-side, making it easy to visualize the differences․ This detailed comparison was crucial in my decision-making process․ I also considered the overall reputation of each lender, looking into online reviews and checking with the Better Business Bureau to ensure they were reputable and trustworthy․ I was surprised by how much the offers varied․ The difference between the highest and lowest interest rates was a significant 1․5 percentage points․ This highlighted the importance of shopping around and comparing offers from multiple lenders․ It was a time-consuming process, but ultimately, it saved me a substantial amount of money in the long run․ The careful comparison allowed me to choose the loan that best suited my financial situation and goals․

Negotiating with the Lender

Once I identified the lender offering the most favorable terms – a local credit union called “Community First” – I didn’t simply accept their initial offer․ I prepared for negotiation․ I had already done my research and knew the prevailing interest rates for similar loans in my area․ Armed with this knowledge, I politely contacted my loan officer, Eleanor Vance, and explained that while I was impressed with Community First’s offer, I had received a slightly lower rate from another institution, though with less favorable terms․ I didn’t lie; I simply highlighted the other offer’s attractive aspects to leverage a better deal․ Eleanor was professional and understanding․ She didn’t immediately match the lower rate, but she listened carefully to my concerns and explored options within their guidelines․ She explained that while they couldn’t match the exact rate, they could offer a slight reduction, along with a waiver on certain processing fees․ This resulted in a monthly payment that was significantly lower than the original offer․ The negotiation process was surprisingly straightforward and collaborative․ Eleanor emphasized that they valued my business and wanted to find a solution that worked for both of us․ The entire experience was far less adversarial than I had anticipated․ I learned that a polite, informed approach, backed by concrete data, can go a long way in securing a better loan deal․ The few percentage points I negotiated off the initial interest rate will save me hundreds of dollars over the life of the loan․ It was definitely worth the effort․

Securing the Loan and My New Car!

After finalizing the terms with Eleanor Vance at Community First, the loan process was surprisingly smooth․ All the necessary paperwork was efficiently handled online, minimizing the need for in-person visits․ I received regular updates via email, keeping me informed of the loan’s progress․ Within a week, the funds were transferred to the dealership, and I was finally ready to pick up my new car – a sleek, silver hatchback I’d been eyeing for months! The feeling of driving away in my own car, knowing I’d secured a fantastic interest rate, was immensely satisfying․ The entire experience, from initial research to finalizing the loan, taught me the importance of careful planning and diligent comparison shopping․ I learned that securing the best interest rate requires more than just applying for the first loan offered․ It involves understanding your credit score, researching different lenders, and being prepared to negotiate․ My patience and persistence paid off handsomely, resulting in significant savings over the life of my car loan․ I even celebrated with a small dinner at my favorite Italian restaurant, “Luigi’s,” to mark the occasion․ The delicious pasta carbonara was the perfect way to end this exciting chapter of my life; The whole process, from start to finish, was a testament to the power of preparation and proactive engagement․ I highly recommend taking the time to thoroughly research and compare options before committing to a car loan․