Credit card debt can feel like a heavy weight, constantly impacting your financial well-being. It’s easy to accumulate, but often difficult to eliminate. The high interest rates associated with credit cards can quickly turn small balances into significant burdens. This article explores effective and strategic approaches to tackle your credit card debt and regain control of your finances, offering actionable steps you can implement today.

Understanding Your Credit Card Debt: A Crucial First Step

Before diving into repayment strategies, it’s essential to understand the specifics of your credit card debt. This involves gathering information about your balances, interest rates, and minimum payments. This knowledge will empower you to make informed decisions and choose the most effective repayment methods.

Gathering Key Information About Your Cards

Compile a list of all your credit cards and note the following information for each:

- Card Balance: The outstanding amount owed on each card.

- Annual Percentage Rate (APR): The interest rate charged on your balance.

- Minimum Payment: The smallest amount you’re required to pay each month.

- Due Date: The date by which your payment must be received.

Strategic Approaches to Credit Card Debt Repayment

Once you have a clear understanding of your debt, you can begin implementing strategic repayment plans. Several methods exist, each with its own advantages. The best approach will depend on your individual financial situation and preferences.

The Debt Avalanche Method: Prioritizing High-Interest Cards

The debt avalanche method focuses on paying off the card with the highest interest rate first, while making minimum payments on all other cards. This strategy can save you the most money in the long run by minimizing interest charges;

The Debt Snowball Method: Building Momentum with Small Wins

The debt snowball method involves paying off the card with the smallest balance first, regardless of the interest rate. This approach provides a quick win and can boost your motivation to continue paying down debt.

Consolidation and Balance Transfers: Exploring Your Options

Consolidating your debt or transferring balances to a lower-interest card can significantly reduce your interest payments and simplify your repayment process.

Debt Consolidation Loans: Streamlining Your Payments

A debt consolidation loan combines multiple debts into a single loan with a fixed interest rate. This can make budgeting easier and potentially lower your overall interest costs.

Balance Transfer Credit Cards: Taking Advantage of Introductory Offers

Balance transfer credit cards offer a low or 0% introductory APR for a limited time. Transferring your balances to one of these cards can save you a substantial amount of money on interest.

- Research: Carefully compare balance transfer offers from different credit card companies.

- Fees: Be aware of any balance transfer fees, which can offset the benefits of a lower interest rate.

- Introductory Period: Understand the length of the introductory period and plan to pay off the balance before the regular APR kicks in.

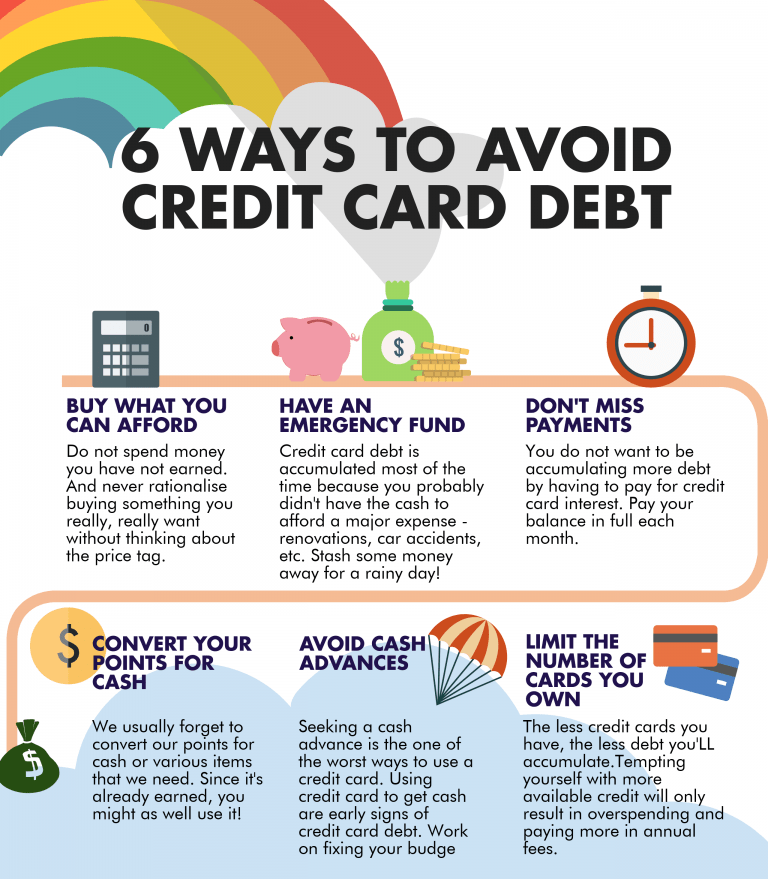

Beyond Repayment: Preventing Future Credit Card Debt

Paying off your credit card debt is a significant achievement, but it’s equally important to prevent future debt accumulation. This requires adopting responsible spending habits and creating a solid financial plan.

Creating a Budget and Tracking Expenses

Developing a budget and tracking your expenses can help you identify areas where you can cut back on spending and allocate more money towards debt repayment and savings.

Avoiding Impulse Purchases and Living Within Your Means

Resisting impulse purchases and living within your means are crucial for maintaining financial stability and avoiding unnecessary debt. Consider implementing a waiting period before making large purchases.

Taking control of your credit card debt is a challenging but rewarding journey. By understanding your debt, implementing strategic repayment methods, and adopting responsible spending habits, you can achieve financial freedom. Remember, consistency is key, and even small steps can make a big difference over time. Don’t be afraid to seek professional help if you’re struggling to manage your debt on your own. Financial advisors can provide personalized guidance and support to help you reach your financial goals.