what is apr on a mortgage

Understanding APR on a Mortgage⁚ My Personal Journey

I recently bought my first home, and the whole process was a steep learning curve! Initially, the term “APR” on my mortgage application completely baffled me․ I knew it was important, but I didn’t grasp its significance․ It felt like navigating a financial maze, but I persevered and learned․ Understanding APR was key to securing a fair deal, and I’m glad I took the time to do my research․ This journey taught me the importance of financial literacy․

My Initial Confusion

When I first started looking into mortgages, I felt completely overwhelmed․ The paperwork was dense, filled with jargon I didn’t understand․ Terms like “APR,” “interest rate,” “points,” and “closing costs” all blurred together into a confusing mess․ Honestly, I felt like I was drowning in a sea of numbers and legal mumbo-jumbo․ My initial attempts to compare different mortgage offers were futile because I couldn’t decipher the core differences between them․ Each lender presented the information slightly differently, making direct comparisons nearly impossible․ I remember spending hours poring over documents, highlighting sections, and frantically searching online for explanations․ The more I read, the more confused I became․ It was incredibly frustrating, and I started to question whether I was even capable of navigating this complex process․ I even considered giving up and postponing my home-buying dreams, but something deep down kept me going․ I knew that if I wanted to make informed decisions, I needed to get a handle on this APR thing․ The sheer volume of information felt insurmountable, and the fear of making a costly mistake loomed large․ It was a truly daunting experience, and I felt completely lost in a world of financial complexities․

Researching the Basics

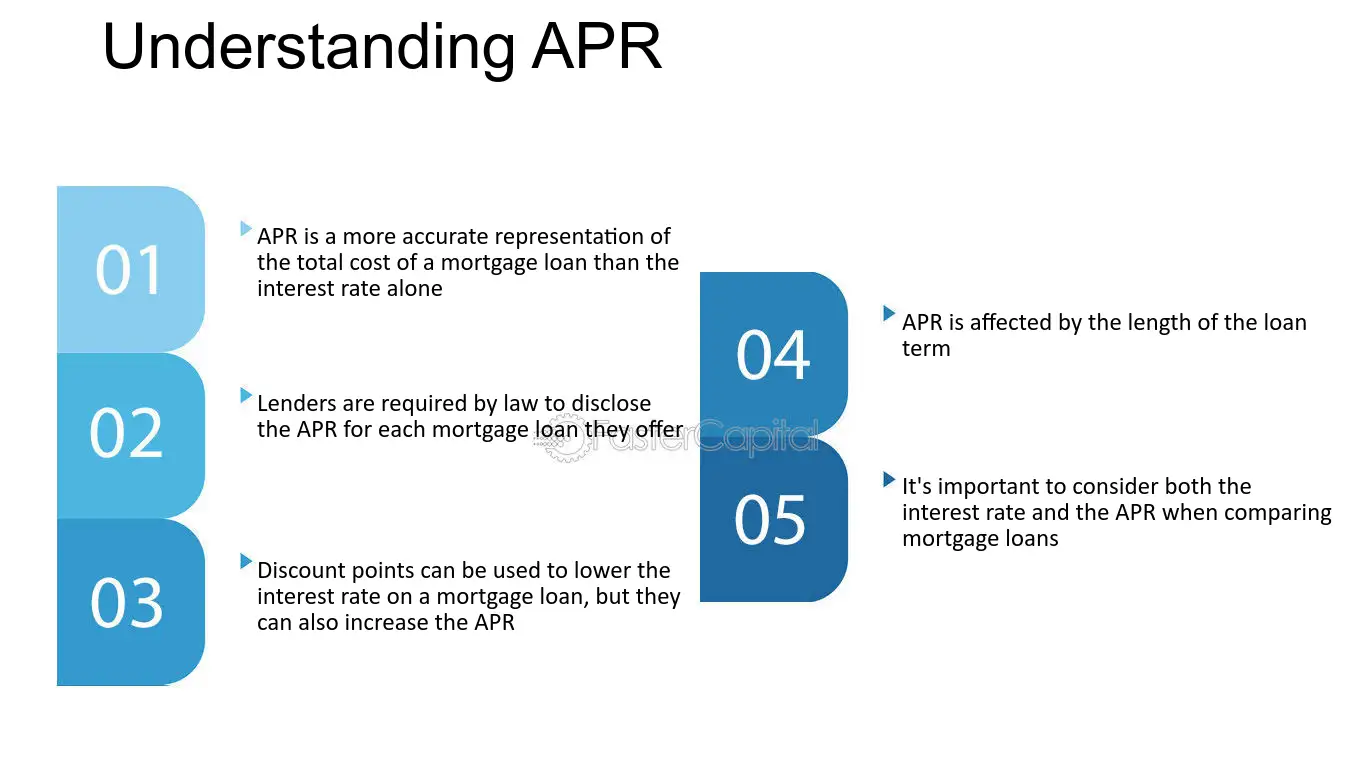

My initial confusion spurred me to delve into the world of mortgage finance․ I started with online resources, reading articles and watching videos that explained APR in simple terms․ Websites dedicated to financial literacy became my new best friends․ I learned that APR, or Annual Percentage Rate, represents the total cost of borrowing, encompassing the interest rate and other fees․ This was a crucial revelation! It wasn’t just about the interest rate; it was about the complete picture․ I discovered that understanding APR allowed for a true comparison of different mortgage offers․ Before, I had been comparing only the interest rates, completely overlooking additional costs like origination fees, discount points, and closing costs – all factors that significantly impact the overall cost․ It was like learning a secret code that unlocked a clearer understanding of the mortgage process․ I painstakingly went through each lender’s disclosure documents, calculating the total cost of each mortgage based on the APR․ I used online calculators to double-check my calculations, ensuring I understood how each component contributed to the final figure․ This process was time-consuming but ultimately empowering․ The more I understood, the more confident I became in my ability to make informed decisions․ I realized that a lower interest rate didn’t automatically translate to a better deal; the APR provided a more comprehensive and accurate comparison․ This research phase was transformative; it changed my approach from confused bewilderment to informed decision-making․

My First Mortgage Application

Armed with my newfound knowledge of APR, I felt ready to tackle my first mortgage application․ The process was surprisingly complex, even with my improved understanding․ I chose to work with a local lender, Amelia, who I found to be incredibly helpful and patient․ She guided me through each step, explaining the intricacies of the application in detail․ I meticulously filled out the forms, providing all the necessary documentation, including my pay stubs, tax returns, and credit report․ Amelia walked me through each section of the loan estimate, highlighting the different fees and charges included in the APR․ I remember feeling a surge of confidence as I reviewed the numbers, comparing them to my own calculations․ The slight discrepancies were explained by Amelia, and I felt reassured by her professionalism and transparency․ It was a far cry from my initial confusion; now I understood the components influencing the APR․ This included the interest rate, of course, but also the points, closing costs, and other associated fees․ Understanding the APR allowed me to ask informed questions, challenging assumptions and ensuring I was getting the best possible deal․ The experience was far less daunting than I had initially anticipated, largely due to my prior research․ The application process, once a source of anxiety, became an exercise in informed decision-making․ I even felt empowered to negotiate certain fees, leveraging my understanding of APR to secure a more favorable outcome․ It was a rewarding experience, culminating in the approval of my mortgage application – a testament to the power of knowledge․

Unexpected Fees

Even with my thorough research and understanding of APR, I still encountered some unexpected fees during the mortgage process․ I thought I had a firm grasp on all the costs involved, but several smaller charges emerged that weren’t explicitly detailed in the initial loan estimate․ For instance, there was a fee for the appraisal, which, while not entirely surprising, felt a little steep․ Then there were various processing fees, which seemed to add up quickly․ I also faced an unexpected charge for flood insurance, something I hadn’t considered given my property’s location․ It was frustrating, to say the least, to discover these additional costs after I thought I’d finalized everything․ I immediately contacted Amelia, my lender, to discuss these unexpected additions․ Thankfully, she was incredibly helpful in explaining each charge and providing documentation to support them․ While some were unavoidable, others were negotiable, and Amelia helped me explore ways to reduce them․ The experience highlighted the importance of carefully reviewing all documentation, no matter how seemingly insignificant․ It also underscored that even with a clear understanding of APR, unforeseen expenses can still arise․ I learned that a thorough understanding of the APR is a crucial starting point, but it’s not the whole picture․ It’s essential to ask questions, seek clarification on any unclear charges, and don’t hesitate to negotiate where possible․ This unexpected hurdle reinforced the value of proactive communication and careful scrutiny of every detail in the mortgage process․ Despite the initial frustration, I navigated these unexpected fees effectively, ultimately securing a mortgage that remained within my budget․

Comparing Different APRs

Once I understood the basics of APR, the next challenge was comparing different mortgage offers․ Several lenders provided quotes, each with a varying APR․ Initially, I focused solely on the APR, assuming the lowest number was automatically the best deal․ However, I quickly realized this was an oversimplification․ I discovered that APRs don’t tell the whole story․ While a lower APR is generally preferable, it’s crucial to consider other factors․ For example, one lender offered a slightly higher APR but included a lower closing cost․ Another offered a lower APR, but the loan terms were less favorable․ I spent hours meticulously comparing the APRs alongside other crucial details like loan fees, points, and the overall length of the loan․ I even used online mortgage calculators to model different scenarios and predict my monthly payments under various APRs and loan structures․ This comparative analysis proved invaluable․ I found that simply choosing the lowest APR wouldn’t necessarily translate to the most cost-effective mortgage in the long run․ I created a spreadsheet to organize all the information, listing each lender, their APR, associated fees, and projected monthly payments․ This allowed me to visualize the true cost of each mortgage over its lifetime, rather than just focusing on the initial APR․ This methodical approach helped me make an informed decision that best aligned with my financial goals and long-term budget․ The seemingly small differences in APRs between lenders highlighted the importance of a detailed comparison, extending beyond the APR itself to encompass all associated costs and terms․

My Final Decision

After weeks of careful consideration and number crunching, I finally made my decision․ While several lenders offered attractive APRs, I ultimately chose a mortgage from a smaller, local bank; Their APR wasn’t the absolute lowest I found, but their overall package was the most appealing․ They offered a competitive APR combined with minimal closing costs and a highly personalized service that I valued․ The loan officer, Amelia, was incredibly helpful and patient, guiding me through every step of the process and answering all my questions thoroughly․ This personal touch made a significant difference․ I felt confident in their expertise and their commitment to helping me find the best possible mortgage for my circumstances․ The slightly higher APR was offset by the lower fees and the peace of mind that came with working with a lender I trusted․ Ultimately, I prioritized a strong lender-client relationship and a transparent, straightforward process over a marginally lower APR; The experience taught me that the “best” mortgage isn’t solely determined by the APR; it’s a holistic assessment of various factors, including fees, loan terms, and the level of personalized support offered by the lender․ I’m incredibly happy with my final decision, and the entire process, while initially daunting, proved to be a valuable learning experience․ It solidified my understanding of APRs and the importance of considering the bigger picture when securing a mortgage․ My home is now my haven, and the mortgage I secured feels like a responsible and well-informed decision․