car equity loans

Car equity loans leverage the value of your vehicle to secure a loan․ This means you borrow money using your car as collateral․ Understanding this concept is crucial before applying․ Responsible borrowing involves careful consideration of your financial situation and repayment capabilities․ Explore all available options and compare interest rates to make an informed decision․ Seek professional advice if needed․

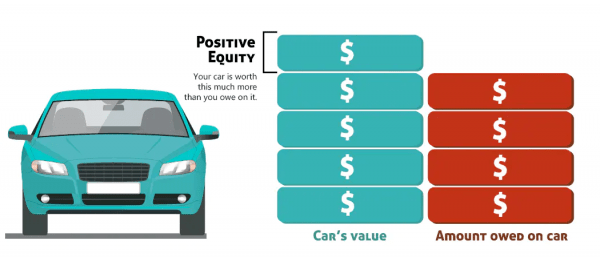

What is Car Equity?

Car equity represents the difference between your car’s current market value and the amount you still owe on your auto loan․ Think of it as the portion of your car you actually own․ For example, if your car is worth $15,000 and you owe $10,000 on your loan, your equity is $5,000․ This equity is a valuable asset that can be used to secure a loan․ Determining your car’s market value is crucial․ You can use online valuation tools, consult with dealerships, or check recent sales of similar vehicles in your area to get a realistic estimate․ Remember, the value of your car can fluctuate based on factors such as its make, model, year, mileage, condition, and overall market demand․ It’s advisable to get multiple valuations to ensure accuracy․ Keeping your car in good condition will help maintain its value and thus, your equity․ Regular maintenance and timely repairs can significantly impact the appraisal of your vehicle․ Failing to do so could decrease your equity and limit your borrowing options․ Understanding your car’s equity is the first step towards securing a car equity loan․ This knowledge empowers you to make informed decisions about your finances․ Accurate assessment of your equity is paramount for a successful loan application․ Don’t hesitate to seek professional assistance if you’re unsure how to calculate your car’s market value․ A clear understanding of your equity will contribute to a smoother and more successful loan process․ Always factor in potential depreciation when assessing your equity․ Cars tend to lose value over time, so it’s important to factor this into your calculations․ By understanding your car’s equity, you can make well-informed decisions about your financial future․

How to Calculate Your Car Equity

Calculating your car equity involves a straightforward process, but accuracy is key․ First, determine your car’s current market value․ Several online resources provide estimated values based on make, model, year, mileage, and condition․ However, these are estimates; consider consulting a local dealership for a more precise appraisal․ They can assess the vehicle’s condition and provide a more accurate valuation․ Next, obtain your loan payoff amount․ This information is readily available on your loan statement, usually online or through your lender’s customer service․ It represents the total amount you still owe on your auto loan․ Subtracting this payoff amount from the car’s market value reveals your equity․ For example, if your car’s worth is $12,000 and you owe $8,000, your equity is $4,000․ This represents the portion of the car you own outright․ Remember, this calculation relies heavily on the accuracy of your car’s valuation․ If you overestimate the market value, your calculated equity will be inflated, potentially leading to complications during the loan application process․ Conversely, underestimating the value could limit your borrowing potential․ Therefore, strive for an accurate valuation․ Consider getting multiple appraisals from different sources to ensure reliability․ Thoroughness in this calculation is crucial, as it directly impacts the loan amount you can secure․ Don’t hesitate to seek professional guidance if you’re unsure about any aspect of the calculation․ Financial advisors or automotive experts can provide valuable assistance․ Accurate equity calculation is fundamental to securing a favorable car equity loan․ By carefully following these steps, you can confidently determine your car’s equity and proceed with your loan application․ Keep in mind that the market value of your car can fluctuate, so regular reassessments might be beneficial, particularly before applying for a loan․ A precise calculation ensures a smooth and successful loan process․

Finding the Right Car Equity Loan

Shop around! Compare offers from multiple lenders, focusing on interest rates and fees․ Consider your credit score’s impact on the interest rate․ Read the fine print carefully; understand loan terms, repayment schedules, and any potential penalties․ A pre-approval can help you gauge your borrowing power before committing․ Don’t rush; choose a lender that best suits your needs․

Comparing Lenders and Interest Rates

Don’t settle for the first offer you receive․ Taking the time to compare lenders and their interest rates is crucial for securing the most favorable car equity loan․ Interest rates can significantly impact the total cost of your loan, so even a small difference in percentage points can translate to substantial savings or added expense over the life of the loan․ Begin by checking with your current bank or credit union, as they may offer preferential rates to existing customers․ However, don’t limit yourself to just one institution․ Explore various options, including online lenders, local credit unions, and traditional banks․ Each lender will have its own criteria for assessing creditworthiness and determining interest rates․ Factors such as your credit score, debt-to-income ratio, and the loan amount will influence the interest rate offered․ Request quotes from several lenders to compare their terms side-by-side․ Pay close attention to the Annual Percentage Rate (APR), which encompasses the interest rate and any associated fees․ A lower APR is generally more desirable․ Remember to factor in any origination fees, processing fees, or prepayment penalties that might be included in the loan agreement․ These fees can add to the overall cost of borrowing, so compare the total cost of the loan, not just the interest rate alone․ Be wary of lenders who offer unusually low interest rates without a clear explanation․ Scrutinize the fine print carefully to avoid hidden fees or unfavorable terms․ By diligently comparing lenders and their interest rates, you can significantly reduce the financial burden of your car equity loan and secure the best possible terms for your situation․ Take your time, do your research, and choose wisely․

Understanding Loan Terms and Fees

Before signing any loan agreement for a car equity loan, thoroughly understand all the terms and fees involved․ This will prevent unexpected costs and financial strain down the line․ Carefully review the loan contract, paying close attention to the loan’s term length․ Longer loan terms generally result in lower monthly payments but lead to higher overall interest paid․ Shorter terms mean higher monthly payments but significantly reduce the total interest paid․ Consider your budget and financial goals when choosing a loan term․ Beyond the interest rate, various fees can impact the total cost of your loan․ These can include origination fees, which are charged for processing the loan application, and prepayment penalties, which are assessed if you pay off the loan early․ Some lenders may also charge late payment fees if you miss a payment․ Understand the implications of each fee and how they will affect your overall repayment plan․ Don’t hesitate to ask questions if anything is unclear․ Clarify the repayment schedule, including the frequency and amount of payments․ Ensure you understand the consequences of missed or late payments, such as damage to your credit score and potential repossession of your vehicle․ If the lender offers different repayment options, such as fixed or variable interest rates, carefully weigh the pros and cons of each․ A fixed interest rate provides predictable monthly payments, while a variable rate may fluctuate over time․ Consider your risk tolerance and financial stability when making this decision․ Review all aspects of the loan agreement meticulously before signing; If you’re unsure about any term or fee, seek clarification from the lender or consult with a financial advisor before committing to the loan․ Taking the time to fully understand the loan terms and fees will safeguard your financial well-being and ensure a smoother repayment process․

Managing Your Car Equity Loan

Successfully managing your car equity loan requires proactive planning and responsible financial habits․ Prioritize timely payments to avoid late fees and potential damage to your credit score․ Set up automatic payments or reminders to ensure you never miss a payment deadline․ Budgeting is crucial; create a realistic budget that accounts for your loan payment alongside other essential expenses․ Track your spending and adjust your budget as needed to ensure you can comfortably afford your monthly payments․ Unexpected expenses can disrupt your repayment plan․ Building an emergency fund can provide a financial cushion to cover unexpected costs without jeopardizing your loan payments․ Regularly review your loan statement to verify that the payments are being correctly applied and that there are no discrepancies․ Report any errors or discrepancies to the lender immediately․ Maintain your vehicle in good condition․ Since your car serves as collateral for the loan, keeping it well-maintained protects your investment and minimizes the risk of any issues arising that could impact the loan․ Regular servicing and timely repairs demonstrate responsibility and can potentially increase your car’s value․ If you encounter financial difficulties that make it challenging to meet your loan payments, communicate with your lender promptly․ Many lenders are willing to work with borrowers facing temporary hardships, offering options like forbearance or loan modification․ Proactive communication can prevent serious consequences, such as loan default and repossession․ Consider exploring additional income streams if you anticipate financial difficulties․ Part-time employment or freelancing can help supplement your income and ensure you can continue to make your loan payments․ Responsible management of your car equity loan not only protects your creditworthiness but also safeguards your vehicle․ By adhering to a disciplined financial plan and maintaining open communication with your lender, you can successfully navigate the repayment process and maintain financial stability․