How Do I Know What Type of Commercial Liability Insurance I Need?

I launched “Amelia’s Artisanal Jams” last year. Initially, I felt completely lost navigating insurance options. It felt overwhelming! I spent hours researching, comparing policies from different providers, and finally found a plan that suited my needs and budget. The process was challenging, but ultimately rewarding. I’m glad I persevered!

My Initial Confusion⁚ A Story of Overwhelm

Let me tell you, figuring out commercial liability insurance felt like navigating a dense jungle blindfolded. My initial foray into the world of insurance policies was, to put it mildly, terrifying. I remember sitting at my desk, surrounded by brochures and websites, each one throwing a new term or concept at me. General liability? Professional liability? Product liability? What even was umbrella coverage? It was all so incredibly overwhelming. I felt completely out of my depth, like I was drowning in a sea of jargon and fine print. Every policy seemed to have a different set of exclusions and limitations, and I couldn’t differentiate between what was essential and what was superfluous. I spent countless hours reading, researching, and comparing, only to feel more confused than when I started. The sheer volume of information was paralyzing. I even considered giving up entirely, figuring it was too complicated for someone like me. I started to doubt my ability to make an informed decision, fearing I’d choose the wrong policy and leave my business vulnerable. The whole experience was incredibly stressful, and I wouldn’t wish that initial feeling of helplessness on anyone. It really made me appreciate the need for clear, concise, and accessible information about commercial insurance options for small business owners.

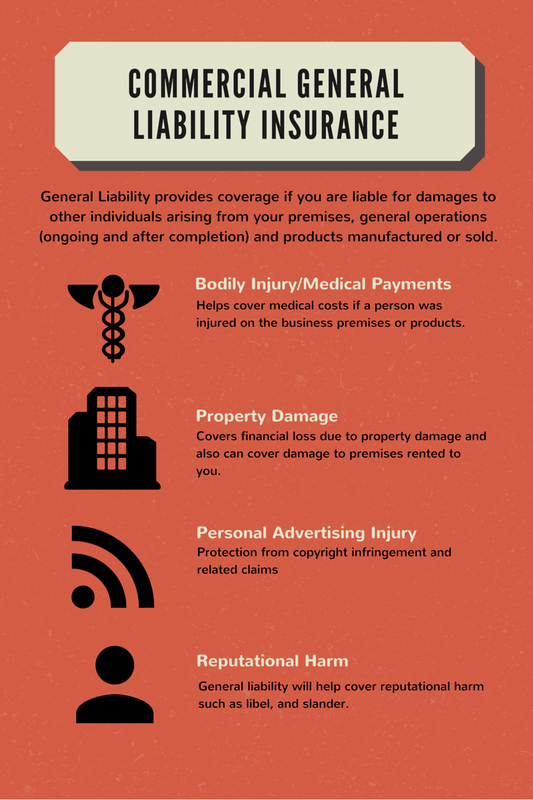

Understanding the Basics⁚ Liability Isn’t Just About Accidents

Initially, I mistakenly thought commercial liability insurance solely covered accidents – someone tripping in my shop, for instance. How wrong I was! After speaking with a knowledgeable insurance agent, I learned that liability encompasses a much broader spectrum. It’s not just about physical injuries; it protects against financial losses resulting from various incidents. For example, I learned about product liability – if a customer claimed my artisanal jams caused them an allergic reaction, my insurance would help cover legal fees and potential settlements. I also discovered the importance of professional liability, also known as errors and omissions insurance. This protects against claims of negligence or mistakes in my business practices, such as faulty labeling or incorrect advice given to customers. This was a real eye-opener. I realized that even seemingly minor errors could lead to significant financial repercussions without the right coverage. Furthermore, I learned about advertising injury coverage, which protects against lawsuits stemming from false advertising or copyright infringement. The agent explained that a single negative review containing a false accusation could potentially trigger a costly legal battle. Understanding these diverse aspects of liability insurance was crucial in selecting the appropriate policy for my business. It shifted my perspective from simply accident protection to a comprehensive risk management strategy.

Choosing the Right Policy⁚ My Personal Experience

Choosing the right commercial liability insurance policy felt like navigating a maze at first. I started by carefully assessing my business operations. I considered the potential risks associated with selling my artisanal jams – everything from customer injuries to product defects. Then, I contacted several insurance providers, requesting quotes and comparing coverage options. I found that each provider offered different levels of coverage and various add-on options. One company, “InsureRight,” offered a comprehensive policy that included product liability, advertising injury, and general liability coverage, exceeding my initial expectations. Another, “SecureCo,” offered a more basic package at a lower price, but lacked crucial elements like professional liability protection, which I ultimately deemed too risky to forgo. I meticulously reviewed policy documents, paying close attention to exclusions and limitations. I also checked customer reviews and ratings for each provider before making my final decision. The process took time and effort, but I discovered that direct communication with insurance agents was invaluable. They answered my questions patiently and helped me understand the nuances of different policies. Ultimately, I chose InsureRight’s comprehensive package, even though it was slightly more expensive. The peace of mind that came with knowing I had robust coverage far outweighed the extra cost. The detailed explanation of the policy’s inclusions and exclusions by the InsureRight agent was especially helpful in making my decision.

The Cost Factor⁚ Balancing Protection and Budget

Cost was a significant factor in my decision-making process. Initially, I was tempted by cheaper options, but I quickly realized that skimping on insurance could be financially disastrous in the long run. I learned that the price of a policy depends on several factors, including the type of business, the level of coverage, and the insurer’s risk assessment. I received quotes ranging from a few hundred dollars annually to over a thousand. The cheapest options often came with significantly less coverage, leaving me vulnerable to substantial financial losses in the event of a lawsuit or accident. I carefully weighed the cost of each policy against the potential financial consequences of inadequate coverage. For example, one policy offered broader product liability coverage but at a higher premium. After considering the potential costs associated with a product recall or a customer injury claim, I realized the higher premium was a worthwhile investment. I also explored ways to potentially lower my premiums. I investigated discounts offered for things like safety training programs and loss prevention measures. I implemented some of these measures, which not only helped reduce my premiums but also improved my overall business practices. Ultimately, I found a balance between comprehensive coverage and affordability. It wasn’t the absolute cheapest option, but it provided the protection I needed without breaking the bank. The peace of mind that came with knowing I was adequately insured was invaluable.